ELLIOTT D. POLLACK

& Company

FOR IMMEDIATE RELEASE

September 16, 2019

The Monday Morning Quarterback

A quick analysis of important economic data released over the last week

Recent events could reduce Saudi oil production in the short term by 5 million barrels per day and reduce world oil production by 5%. This is a big number. Oil markets are thin and small shifts in the supply/demand equation have significant effects on price. A major shift like this one could have significant effects on price. By the time you read this, on Monday, you will have a better idea of the impacts than I do writing this on Sunday. Even if the Saudi’s statements about getting most of the production back on line quickly is true, prices could still move significantly. Plus, now that the Houthi rebels have crossed the line in terms of attacking Saudi oil fields, who is to know when it might happen again. This will also be counted into price.

The U.S. is closer to being energy independent than ever before, but, while we are now exporters of oil, we are importers as well. We have a refining problem, not a production problem. Much of the refining capacity in the U.S. was built when we were more reliant on imports and were built to refine heavy Saudi oil, not Texas light sweet. This means that prices in the U.S. will be affected. Higher prices for oil and oil products will mean that people will be spending more on oil related products and will have less for other spending. In a slowing economy already facing challenges from slower growth in Europe and China, trade issues and slowing business investment, this type of unexpected event can only be a negative. Consumers, the major strength of the U.S. economy at the moment, will be most affected.

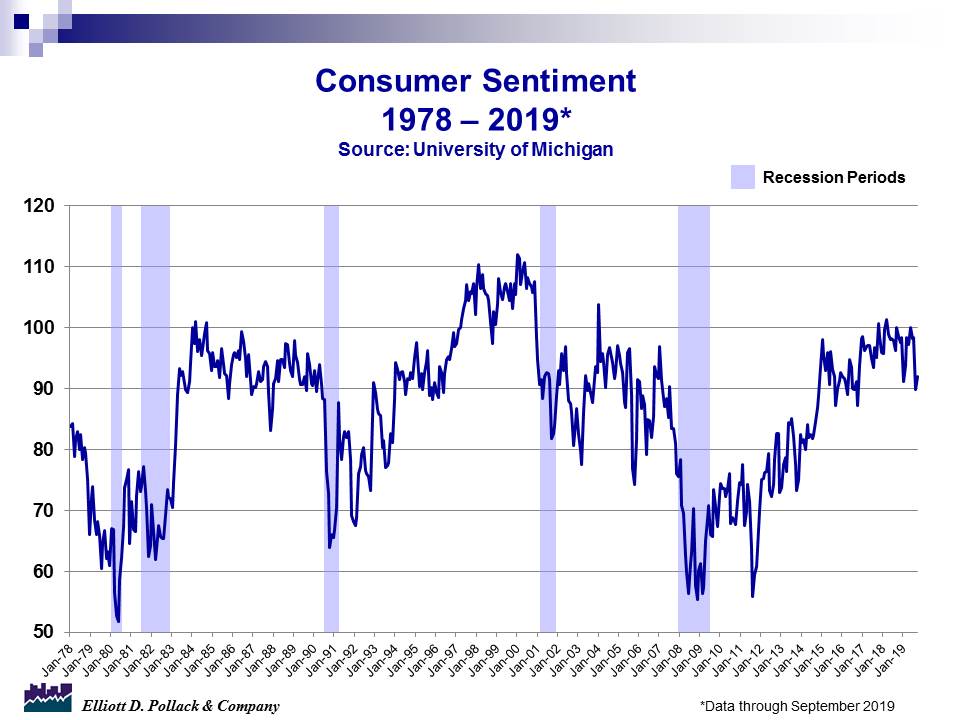

It was an interesting week for economic data. Retails sales were strong in August. That’s especially impressive after an extremely robust July. In examining the data, retail sales in August were fueled by a very strong showing in auto sales. In sectors other than autos, though, retail sales were moderate to weak. But, for consumers to be worried about the future and still purchase lots of new autos really would be unusual. In that regard, the sharp decline in the August consumer sentiment numbers rebounded modestly in preliminary September readings. This is worth watching as either retail sales will slow or consumer sentiment will increase.

In other news, consumer prices less food and energy, generally called the base rate of inflation, were up at their most rapid rate (year over year) in years. This will make the Fed’s Wednesday decision on interest rates a little more interesting. The odds, though, still favor at 25 basis point rate cut this week. The Blue Chip consensus forecast for real GDP still shows the economy growing in 2020 but at a slower rate than this year. However, 38.3% of those polled believe there will be a recession next year. This is up from 36.6% last month. Growth in Europe (or lack thereof), Brexit, China and trade uncertainties were developments raised as concerns. This should give the FED cover for the rate cut.

In other news, the number of unfilled jobs in the U.S. was only modestly lower than last month but was still at a very high level by historic standards. Consumer credit expanded rapidly. And total manufacturing and trade sales grew modestly.

U.S. Snapshot:

The September Blue Chip economic consensus forecast for Real GDP suggests that real GDP will grow by 2.3% this year and 1.8% next year. Major issues discussed by the panel included and increased recession probability for next year, the U.S.-China trade dispute, greater uncertainty concerning business investment and supportive monetary policy worldwide. Other issues that would be problems for the U.S. economy include the slowdown in Europe, Brexit and China uncertainties.

The number of unfilled job openings was little changed. There were 7.2 million unfilled jobs as of the last day of July. That’s about the same number as the end of June and 3.0% fewer than a year ago.

The University of Michigan consumer sentiment index posted a small rebound after the sharp decline in August. The September preliminary reading was 92.0 compared to 89.8 in August and 100.1 a year ago (see chart below).

Consumer credit increased at a 6.8% annual rate in July and is now 5.2% above year earlier levels. In July, it was revolving credit (primarily credit cards) that rose rapidly. Revolving credit increased at an 11.2% annual rate and was 4.6% above year earlier levels. Non-revolving credit, mainly auto and student loan debt, rose at a 5.3% annual rate and stood at 5.4% above year earlier levels. Overall, the increase was the largest since last July and the fastest pace of growth in revolving credit since November 2017. This could mean one of two things: either consumers are using revolving credit more because they lack the cash to cover spending on basic needs or consumers are using revolving credit more because they feel confident about repayment capabilities due to feelings of job security. Given the current growth of the economy, the expansion of consumer credit in July is apt to be taken at face value as an encouraging sign.

The consumer price index for all urban consumers (CPI-U) increased 0.1% in August and now stands 1.8% above a year ago. But, the CPI less food and energy (the base rate of inflation) increased by 0.3% (a 3.1% annual rate) and is now 2.4% above year earlier levels. See the opening commentary for our thoughts on this.

Retail sales for August rose 0.4% compared to July. In July, retail sales grew at a rapid 0.8%. This is two good months back to back. Yet, in August, except for auto sales, retail sales were flat. Sales from furniture stores, gas stations (mainly due to lower oil prices), clothing stores, restaurants and general merchandise contracted. This could be troubling. Time will tell.

About EDPCo

Elliott D. Pollack & Company (EDPCo) offers a broad range of economic and real estate consulting services backed by one of the most comprehensive databases found in the nation. This information makes it possible for the firm to conduct economic forecasting, develop economic impact studies and prepare demographic analyses and forecasts. Econometric modeling and economic development analysis and planning are also part of our capabilities. EDPCo staff includes professionals with backgrounds in economics, urban planning, financial analysis, real estate development and government. These professionals serve a broad client base of both public and private sector entities that range from school districts and utility companies to law firms and real estate developers.

For more information, contact –

Elliott D. Pollack & company

7505 East Sixth Avenue, Suite 100

Scottsdale, Arizona 85251

480-423-9200