By Pollack

The Fed is of two minds, and we finally got to see just how divided it is. The minutes of the June meeting show a Federal Open Market Committee that cannot agree on where interest rates go from here. Of the eighteen officials who submitted rate projections, nine penciled in at least one increase before the end of the year, eight expected no change at all, and one looked for a cut. On the question that matters most to borrowers, the committee is split right down the middle.

The rate decision itself was old news. What the minutes added was the argument behind it, and the argument is a real one. The Fed has two jobs, stable prices and maximum employment, and for most of this expansion those goals pointed in the same direction. They no longer do. Inflation has proven sticky, which argues for holding rates where they are or nudging them up. But the job market isn’t in great shape, which argues for cutting. The hawks worry that standing pat becomes a mistake if prices reaccelerate. The doves worry the Fed is already too tight for a labor market that is plainly softening. Both camps are looking at the same data and reaching opposite conclusions.

Markets are not waiting around for a resolution. The 10-year Treasury yield, which the Fed does not set but heavily influences, has drifted up to about 4.5% from 4.13% in February. Long-term rates have risen even as the Fed has stood still, which tells you bond investors are not betting on cuts any time soon. Homebuyers felt it. On Thursday the 30-year mortgage rate came in at 6.49%, up from 6.43% a week earlier and back near the top of its range for the year after dipping under 6% in late February. Existing home sales, reported the same morning, slipped 2.4% in June to a 4.09 million annual pace. As the National Association of Realtors’ chief economist put it, the back-and-forth in monthly sales shows just how sensitive buyers are to affordability. The cost of a mortgage follows the bond market, not the Fed’s press release.

So where does this leave us? Waiting, mostly. The Fed meets again on July 28th and 29th, and between now and then it will get two more releases of inflation data, beginning with the June Consumer Price Index on Tuesday. We anticipate another decision to hold rates where they stand. And if there is a decision to change the interest rate, we would expect a hike, not a cut.

U.S. Snapshot

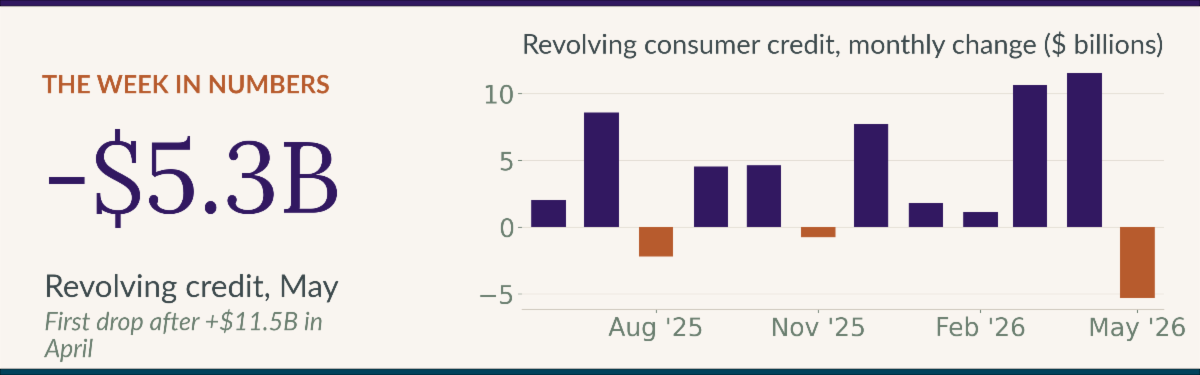

Consumers stopped borrowing in May. Total consumer credit fell $182 million, its first monthly decline since June of last year, and a long way from the $17.5 billion increase economists expected after April’s $20.8 billion gain. The pullback was in the plastic: revolving credit, which is mostly credit cards, dropped $5.3 billion at a 4.7% annual rate, its largest monthly decline in at least a year, after rising $10.7 billion in March and $11.5 billion in April. Nonrevolving credit, which covers auto and student loans, still grew at a 1.6% rate. One month is not a trend, and some of this may be households paying down balances with tax refunds. But a consumer who stops reaching for the credit card is a cautious consumer, and that fits a job market where hiring has clearly slowed. This bears watching.

Existing home sales fell 2.4% in June to a seasonally adjusted annual rate of 4.09 million, giving back most of May’s gain, though sales remain 2.8% above a year ago. The median existing-home price rose to $440,600, up 1.8% from a year ago and the 36th consecutive month of annual price increases. Affordability has improved from last year, with the Realtors’ affordability index at 102.3 against 95.5 a year ago, but prices keep grinding higher while sales go nowhere.

The service side of the economy kept growing in June, just a touch more slowly. The ISM Services index eased to 54.0 from 54.5 in May, still its 24th straight month above 50, the line that separates expansion from contraction. New orders (55.1) and business activity (55.4) stayed solid, and the employment index rose to 51.2, its first reading in growth territory in four months. The prices gauge fell to 67.7, its lowest since February, a welcome sign on the inflation front even as it says costs are still climbing.

Initial jobless claims fell to 215,000 in the week ending July 4, down 2,000 from the prior week and a bit better than the 218,000 economists expected. The four-week average dropped to 218,750 and continuing claims edged up to 1.81 million. Layoffs remain low even as hiring has slowed, which is the central puzzle of this labor market.

The 30-year fixed mortgage rate rose to 6.49% in the week ending July 9 from 6.43% a week earlier, though it is still below the 6.72% of a year ago. Rates began the year at 6.16%, bottomed at 5.98% in late February, and have climbed steadily since.

Arizona Snapshot

Light week for Arizona data. The state’s marquee reports all land next week, so the local read this week comes through the national numbers.

The move in mortgage rates is unwelcome news for a Greater Phoenix housing market that has already cooled. The 30-year rate is now a full half point above its February low, national existing home sales slipped 2.4% in June, and metro Phoenix prices have been among the softest of the large U.S. markets in recent readings. Affordability remains this market’s central problem, and this week it got slightly worse rather than better.

For Arizona buyers and builders, the Fed’s standoff means the relief of lower borrowing costs is still on hold. Until the committee settles its internal debate, mortgage rates will keep taking their cues from the inflation reports rather than from the Fed’s target rate. That makes Tuesday’s Phoenix-area and national inflation readings the ones to watch here at home.