By Pollack

The Federal Reserve did exactly what almost everyone expected last week, and then it did something many did not. On Wednesday, June 17, the Fed held its target range for the federal funds rate at 3.50 to 3.75%, a unanimous decision and the first under new Chairman Kevin Warsh. That part was expected. The surprise was in the projections. For the first time in this cycle, the median policymaker stopped penciling in a rate cut for 2026. Back in March, the typical official still saw the year ending around 3.4%, which implied one more quarter-point cut. As of last week, the median moved up to roughly 3.8%, which implies no cuts at all this year, and potentially a reversal to a rate hike.

The reason is no mystery. Inflation has been drifting the wrong way, running near a three-year high, and the Committee said plainly that it wants to see prices moving convincingly back toward its 2% goal before it eases. In the new projections, 17 of the 18 officials judged the risks to inflation to be tilted to the upside. When that many people around the table are worried about the same thing, policy rarely loosens. So the message from this meeting was less about the rate itself, which did not move, and more about how long it is likely to stay where it is.

It is worth a word on what the projections actually are. The so-called dot plot is simply a chart, and each official marks where they expect interest rates to be at the end of the next few years. It is not a promise, and it is not a vote. It is a snapshot of opinion that can shift with the next few data points. But the direction of the shift matters, and the direction since March has been clear: higher for longer. Chairman Warsh was careful not to slam any doors, but he left little doubt that the Committee is in no hurry.

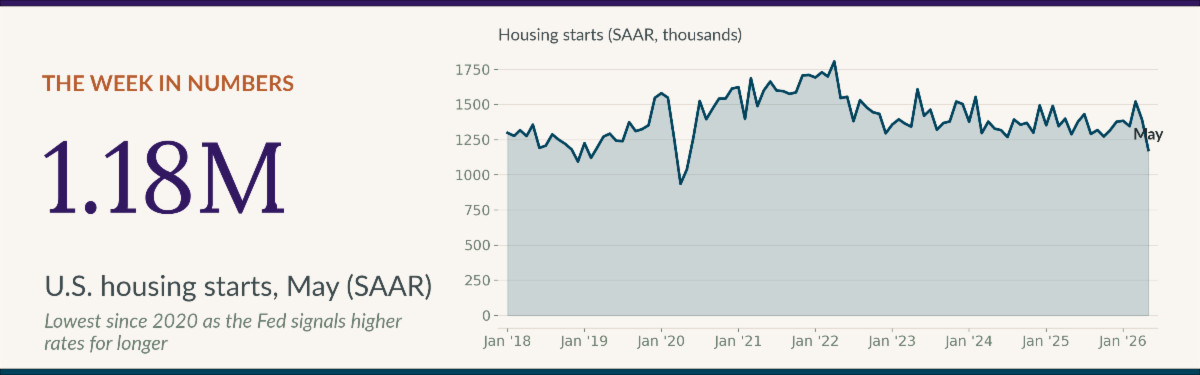

The rest of the week’s data showed an economy that is splitting in two. The consumer, remarkably, is still spending. Retail sales rose 0.9% in May, nearly double what forecasters expected and the eighth straight monthly increase, and initial claims for unemployment held at a low 226,000. But the rate-sensitive part of the economy is buckling. Housing starts fell more than 15% to their slowest pace since 2020, builder confidence sat near a multiyear low, and permits drifted lower as well. Higher for longer is a manageable message for a household with savings and a job. It is a much harder message for housing and other real estate sectors.

So where does this leave us? The Fed has told us plainly that it is in no hurry, and the housing numbers show what that stance costs. The next meeting is July 28 and 29, and between now and then the June inflation report, due in mid-July, will matter a great deal. If price pressures ease, the conversation can turn back to when the Fed will cut. If they do not, that conversation gets pushed further out. We do not expect a return to rate hikes yet, but anyone hoping for cheaper money before the leaves turn should probably settle in for a longer wait. This bears watching.

U.S. Snapshot

- The Fed held the federal funds target at 3.50 to 3.75% on June 17. Its new projections lifted the median year-end 2026 dot to about 3.8% from 3.4% in March, erasing the rate cut officials had previously expected.

- Retail sales rose 0.9% in May, the eighth straight monthly gain, and stand 6.9% above a year ago.

- Industrial production was nearly flat in May, edging up 0.1% after a 0.9% jump in April and standing 1.7% above a year ago. Manufacturing output was unchanged and capacity utilization held at 76.2%.

- Housing starts fell 15.4% to a 1.177 million annual rate, the slowest pace since May 2020 (single-family starts down 1.9% to 882,000), while building permits were steadier, easing 0.7% to a 1.413 million rate.

- The NAHB/Wells Fargo builder confidence index slipped two points to 35 in June, a 14th straight month below 40, with 35% of builders cutting prices.

- The Conference Board’s Leading Economic Index rose 0.1% in May to 99.3, its second straight monthly gain, but its six- and twelve-month growth rates remained negative, still pointing to slower growth ahead.

- Initial jobless claims were 226,000 in the week ending June 13, down 4,000; continuing claims rose 24,000 to 1.81 million.

Arizona Snapshot

- Arizona’s job market cooled but kept growing in May. According to the state Office of Economic Opportunity’s report released June 18, Arizona added 16,000 nonfarm jobs over the past year, a 0.5% gain, to about 3.28 million, edging the national pace of 0.3%. Health Care and Social Assistance (up 15,900) and Professional and Business Services (up 9,400) led the gains, while Financial Activities (down 5,200) and Leisure and Hospitality (down 4,700) lagged.

- The state’s job growth remained concentrated in Greater Phoenix, which added 23,600 nonfarm jobs over the year, up 1.0%, to about 2.48 million, with an unemployment rate of 4.1%. Greater Tucson was essentially flat, adding just 100 jobs (0.0%) to 407,400, with unemployment at 4.7%. Phoenix continues to lead the state in job creation, as it has through most of this expansion.

- The softer note in the report was the unemployment rate, which edged up to 4.8% on a seasonally adjusted basis in May from 4.7% in April, above the national rate of 4.3%. More telling, Arizona’s labor force also shrank over the past year, down 49,805 people or 1.3%, a clear change from the growth of recent years, and a softening labor market signal. We will be watching whether that is a blip or the start of a trend.

- Greater Phoenix housing is still bumping along the bottom of a four-year slowdown, in the words of Jim Daniel of RL Brown Reports (RLBrownReports.com). Greater Phoenix resales totaled 6,664 in May, up 3.9% from a year ago, while new-home closings fell 13.4% to 1,844 and single-family permits slipped 5.8% to 1,578. The median resale price held flat from a year ago at $450,000 and the median new-home price eased 1.4% to $483,622. Daniel notes that May 2026 looks much like July 2022, with mortgage rates expected to stay elevated through 2026 and into early 2027.

- Greater Tucson is following the same script, according to RL Brown Reports’ Tucson-Southern Arizona Housing Market Letter (RLBrownReports.com). May resales were essentially flat at 1,384 (down 0.4% from a year ago), while new-home closings rose 1.8% from a year ago to 337 and topped their prior-month level for the first time since June 2025. Permits came in at 259, down 6.8% from a year ago but up 12.1% year to date. The median resale price was $349,950, down 1.4% from a year earlier.

- The common thread is the same one driving the national data: mortgage rates stuck in the mid-6% range and little prospect of near-term relief after last week’s Fed meeting. Arizona still outgrows most of the country on jobs, but until financing costs come down, the for-sale housing market is likely to keep grinding sideways.